Exclusive Residences Observatory - Second Half 2024 - Press Release

Buying and selling: a two-speed market

In the second half of 2024, the Top and Luxury segments (over €3 million and €6 million, respectively) excelled in terms of transactions closed and prices achieved, driven by foreign UHNWIs coming to Milan for the tax benefits guaranteed by residing in Italy. In some cases, owners gave in to direct offers at a price level that "could not be refused." But this niche is very small and involves only a handful of homes sold.

In contrast, in the numerically more relevant, middle range (1-3 million), a predominantly domestic and replacement market, very little is happening. Where foreigners do not drive, there is a problem: homes on the market struggle to find motivated and quick buyers. Procrastinating attitudes - undecided and bewildered - prevail among them: the "excuses" for delaying the purchase may relate from time to time to certain imperfections in the house, the amount and expected timing of renovations, uncertainty about the correct price to offer. Owners who wish to close must accept substantial discounts to convince buyers and speed up decisions.

Average prices up slightly, new records for top homes

Average asking prices continue to rise, but moderately (0.8 percent); the last significant increase in selling prices was in 2019 (+5.5 percent). Over the past five years, growth has been gradual and stable.

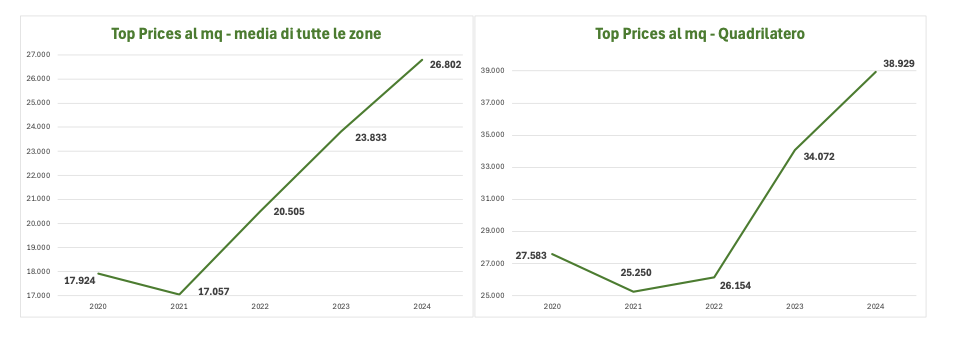

On the other hand, the maximum prices per square meter of the most valuable houses put on the market have grown a lot: almost 50 percent since 2020 in the city average. In Quadrilatero, this value reached almost 39,000 euros, confirming the area as the most exclusive and expensive in the city.

Leases: demand up sharply and rents on the rise

Demand is robust in all zones and segments. In the Top one (over 100,000euro annually), supply is failing to meet demand, with an even more pronounced deficit for rentals above 200,000 euros (Luxury bracket). The few residences of high aesthetic value have already been absorbed by new residents who have arrived to take advantage of the tax benefits. In the lower price brackets, supply has increased, but remains insufficient to cover continued high demand, keeping the market under pressure.

IN DETAIL.

Purchases and sales

Supply and Demand: in the second half of 2024, the market for exclusive residences in Milan confirmed a well-established trend: a clear separation between the top and middle tiers, with increasingly divergent demand and price dynamics.

"The higher brackets continue in a very positive trend, driven by strong international demand, driven in part by the imminent expiration of "non-dom" tax breaks in the UK (April 2025). This dynamic has led many international families to move to Milan, with 80 percent of real estate inquiries targeting the city. On the other hand, the intermediate bracket, composed mainly of Italian buyers, remains characterized by great caution in purchases, often waiting for a better offer." commentsGabriele Torchiani, senior partner and head of ORE.

Further complicating the picture is the wide variability of prices per square meter, with homes exceeding 25,000 euros/m² and others not reaching 7,000 euros/m², making it difficult to determine what is the correct value for making an offer. This disparity is easily explained: the most expensive homes are already renovated, bright, located on the upper floors of elegant and well-maintained buildings. Those at lower prices, on the other hand, are located on lower floors, need renovation work, and have less attractive features, such as penalizing overlooks or unrational space distributions. Properties with more critical features tend to remain on the market for a long time or end up being converted into small apartments for short-term rental.

Another restraint for buyers is the fear of falling prices in the medium term.However, this concern appears unfounded: the value of a high-quality residence in Milan's exclusive areas has now steadily exceeded 10,000 euros/m² and will continue to rise in the long term, aided by the chronic shortage of supply in a city with limited area.

Also confirming the strength of the market is the UBS Global Real Estate Bubble Index, which in its September 23 report ranks Milan among the cities with the most balanced market and lowest bubble risk in Europe, second in the world only to São Paulo, Brazil.

The absorption index grew slightly by 0.6 percent,settling above 20 percent, but remains far from the record levels of 2022(27.5 percent). In the domestic market, dominated by replacement demand, properties with unconvincing quality characteristics remain unsold. In fact, potential buyers are unwilling to compromise on quality and often suspend their search, discouraged by the lack of really good solutions.

A determining factor in the rate of absorption is the initial sale price:many homes enter the market with valuations that are excessive compared to their actual characteristics. This phenomenon depends mainly on owners who, influenced by transaction values in the Top/Luxury or new segment, force their hand toward unrealistic valuations. The result? These properties remain unsold for a long time, accumulating a history of failure and suffering repeated declines, which end up further lengthening buyers' decision-making time.

In line with the observed dynamics, the average closing time for purchases and sales continues to lengthen slightly, reaching nearly 7 months (6.8). At the same time, the average discount widens further by 0.5 percent,to 7.2 percent-an increase of one percentage point year-on-year.

"The market in the Luxury segment remains dynamic, sometimes with exceptional performance in terms of prices and rents per square meter, but it is an enormously smaller market than the non-expert public imagines. The incomplete digitization of deeds of sale and purchase does not allow us a panoramic view of the market, but according to our analysis in 2024 in Milan in the 5 exclusive areas we analyzed no more than 100-150 houses over 250 sqm were sold, which become 60-70 over 300 sqm. To give a yardstick of comparison, suffice it to say that in the week between February 24 and March 2 in Manhattan 42 homes above $3 million were sold in the neighborhood south of 96th Street alone." commentsMarco E. Tirelli. "At the same time for the first time in history maximum rents per sq. m. for Luxury residential exceeded those for office in the city's CBD (Central Business District). Compared to 800 euros per sqm in the locations most desired by companies and large professional firms, in fact, rental homes are well above 1,000 euros."

The average time that unsold residences have been on the market has dropped by more than a month, but this is mainly due to the withdrawal of "exhausted" properties, i.e., those that have been without buyers for a long time. Despite this, the absolute value remains very high, exceeding two years.

Asking prices continue to show moderate rises, with an increase of 0.8 percent for the average price and +1 percent for the average maximum price. However, behind this general trend lies, as indicated above, a relevant phenomenon: in the Luxury segment (over 6 million euros), maximum prices per square meter have increased markedly, driven by high demand from international buyers, particularly UHNWIs leaving the UK for tax reasons.

The level of average prices is of no particular concern. This is because their growth follows a healthy and sustainable dynamic, with no signs of excessive speculation. Moreover, Milan continues to strengthen its attractiveness, both for those who choose to settle there and for investors looking for solid assets capable of guaranteeing adequate returns and maintaining their value in the medium to long term. Instead, the problem lies in the circumstance that at the average price level, the market does not have a sufficient stock of good quality homes, a circumstance that tends to push up the prices of the few good homes.

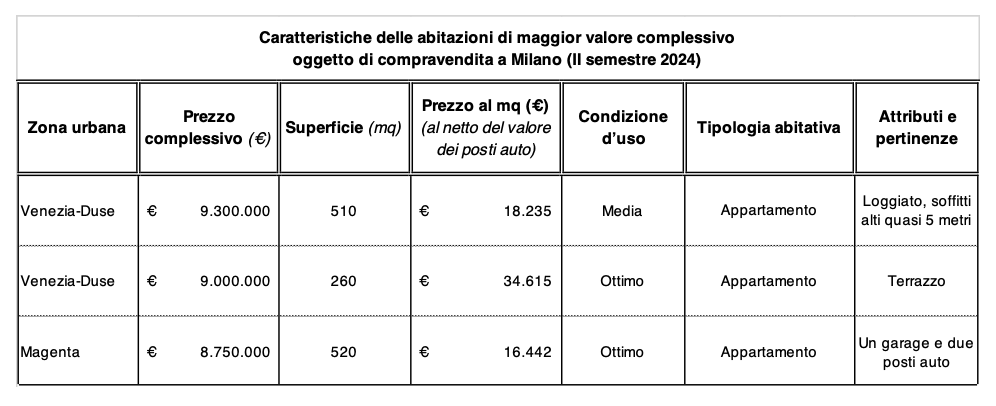

The volume of the three largest sales in the six-month period exceeded 27 million euros, with values ranging from 16,400 to 35,000 euros/m².

The leases

The rental market for exclusive residences in Milan continues to experience a strong increase in demand in all areas and segments. Potential tenants are exclusively looking for recently renovated, furnished or semi-furnished (with kitchen and cabinets) properties. Demand is still dominated by secondary demand, i.e., those who need a temporary solution, often waiting to buy a home but unable to find the right option right away. This segment includes both Italian and foreign residents and expats returning to Italy for work or tax reasons.

Primary demand, related to longer-term needs, also maintains a stable trend, but with a well-established feature: although contracts are formally 4-years with a renewal option, their actual duration tends to be much shorter.

"In the Top segment (more than 100,000 euros per year, excluding expenses), demand far exceeds supply, with an even more pronounced deficit for apartments with annual rents above 200,000 euros (Luxury bracket). The few perfect residences with high aesthetic and scenic value have been absorbed by the recent wave of new residents moving to Milan for tax reasons," Torchiani adds.

In the lower price ranges, thesupply of rental apartments has increased but still struggles to meet such high demand, keeping the market under pressure.

The absorption rate is slightly increasing over the six-month period, reaching 36.8 percent. The Brera, Magenta and "Other areas" areas exceed 40%, while in other areas the absorption rate is lower, penalized by the presence of properties that have not been upgraded or are perceived as inadequate by the most demanding tenants.

The average rental time is decreasing, returning to an all-time high in the first half of 2023 with 3.5 months. Valuable, well-renovated properties find a tenant quickly and, in some cases, are leased before renovations are even completed.

The average discount applied to asking rents stands at 4.5 percent, with a clear differentiation between properties of different qualities. The most exclusive residences, for which owners receive more than one offer, are rented without any price reduction, while for second-tier properties the discount can be as high as 10 percent. For properties that stay on the market longer, the average time on the market rose to 9.6 months.

Rents continue their moderate growth, with an average increase of 0.32 percent in the second half of 2024. Top rents-that is, the maximum rent per square meter per individual residence-reach extraordinary levels, exceeding 600 euros throughout the city, with peaks of 1,200 euros in the Quadrangle. This growth is fueled by the scarcity of supply, the high quality of available properties, and demand from international tenants, who are used to paying similar figures in their home countries.

Forecast for 2025

BUYERS: In the Mid-range segment (1 to 3 million), demand and the number of transactions do not suggest any improvement. The international political situation and general economic climate are not positive, and this has always been a strong brake on investment decisions. The Top segment (3 to 6million) and the Luxury segment (over 6 million), will continue to be characterized by good international demand and extremely limited supply, so it is plausible to expect further increases in sales prices. However, since transactions in this segment represent a marginal share of the overall market, any increases will have no impact on overall price averages.

Looking at the market as a whole, the quantity and quality of supply will continue to be the main determinants. For this reason, we expect substantial stability in the number of transactions in the short term.

RENTAL: Demand for leases will remain high and will also grow further as a result of the secondary component, i.e. from those waiting to buy their city residence and unable to find it turn to the rental segment. However, the lack of supply will make it impossible to increase the number of leases, especially in the Luxury segment. Rents will continue to grow with a moderate trend in the average, while new records are in sight in the Luxury segment.