Exclusive Residences Observatory - Second half of 2025

2025 SPACE ODYSSEY: MILAN IN SEARCH OF A NEW BALANCE

Sales: quality wins, the rest languishes

The market for exclusive residences in Milan continues along a path of substantial continuity compared to the first part of the year, confirming the clear segmentation between the Top and Luxury segments (3-6 and 6+ million respectively), supported by international demand, and the Middle segment (1-3 million),which is mainly domestic and characterized by a cautious and selective approach.

Foreign demand, while remaining high, shows further normalization compared to the peaks of the previous two years. Interest in this demand is increasingly focused on properties with very high location and finish characteristics.The supply available in this segment remains limited and partly consists of properties with quality/price expectations that are not consistent with the needs of potential buyers.

The average absorption rate improved slightly, settling at 21.3% (+1.7 percentage points). The figure is particularly favorable in areas such as Quadrilatero, Centro Storico, and Venezia-Duse, while Brera and Magenta are experiencing greater difficulties.

The average time to sell has fallen slightly to 7 months, but the discount between the asking price and the final price continues to grow, reaching 8.6%. The average time unsold properties remain on the market has fallen below 26 months, but remains very high.

Asking prices confirm the trend since 2021, with fractional increases of around 1% per year: +0.85% for the average price. New and renovated properties (+0.9%) performed better than used properties (+0.75%).

Significant factor: while asking prices rose by 1.5% year-on-year, actual closing prices rose by a modest 0.1%, reflecting a 1.4% increase in discounts over the year.

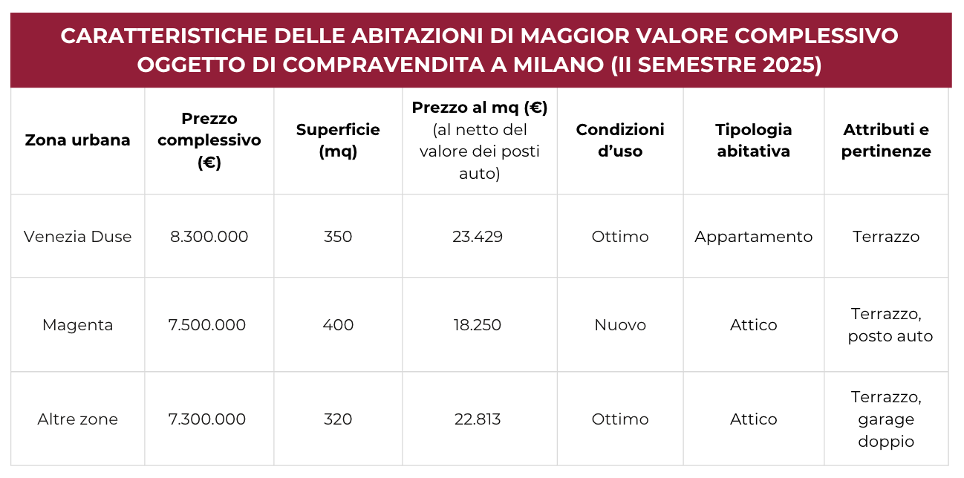

The total value of the three most significant sales in the first half of the year exceeded €23 million, with prices per square meter ranging from €18,000 to over €23,000. Just five years ago, in the second half of 2020, these values ranged from €10,900 to €13,800 per square meter.

The average Top Price in the city (i.e., the highest price per square meter requested in each area of the report) continues to grow, albeit at a slower pace, evolving toward a phase of greater equilibrium.

Rentals: scarcity driving up rents

After years of almost uninterrupted growth, demand has begun to normalize across all segments—Mid-range (40-90k per year plus expenses), Top (90-170k), and Luxury (170+k). This is a natural readjustment following the post-pandemic expansion phase.

The supply of high-quality residences has become even scarcer: many of the best options have already been snapped up by the wave of new residents arriving in 2023-2024.

The absorption index rose to 35.6% (+0.8%), but this figure can be misleading: in reality, both contracts concluded and supply have fallen, with the latter contracting more rapidly.

The average time to rent has fallen slightly to 3.8 months (-0.4%), but only thanks to high-end properties that are snapped up in a matter of weeks. The average discount has fallen to 5.2% (-0.6%). In the mid-range segment, if the contract is not closed within 3-4 months, the reduction in rent can exceed 10%. The vacancy rate for empty apartments extends beyond 10 months.

Rents continue to grow at a controlled rate (+0.64%). Top rents exceeded €750/sq m/year across the entire city, with exceptional peaks of up to €1,100 in the Quadrilatero district.

IN DETAIL.

Purchases and sales

In the second half of 2025, the market for exclusive residences in Milan continued along a path of substantial continuity compared to the first part of the year, confirming the clear segmentation between the higher segments and the intermediate segment. The Top (over €3 million) and Luxury (over €6 million) segments continue to be driven mainly by international demand, while the Middle (€1-3 million) segment, fueled almost exclusively by domestic buyers, remains characterized by a cautious and selective approach.

"However, the current trend seems set to gradually reduce this differentiation," comments Gabriele Torchiani, senior partner and head of ORE - Although we will have to wait until at least 2026 to have adequate comparative data, there appears to be a decrease in foreign demand, which, while remaining well above supply, shows a normalization compared to the peaks recorded in the two-year period 2023-2024. "

At least three factors justify this impression: i) the end of the exodus from London following the cancellation of tax benefits for "res non dom" (starting April 6, 2025); ii) the increase in the flat tax from the original €100,000 to the current €300,000; iii) the structural shortage of exclusive residences in the city.

"At the moment, data on the number of applicants for tax breaks defined as 'flat tax' are not yet available for either 2025 or 2024, " says Marco E. Tirelli , "but the feeling is that the peak was reached in 2024 and that by 2025, levels will have returned to 15-20% lower. Assuming approximately 1,400-1,500 main applicants for 2024, in 2025 this would correspond to a number between 1,100 and 1,200, which would bring it back to the 2022 level (1,136)."

However, this reduction in the number of new residents seems to correspond to an increase in the quality of the homes in demand, which are increasingly concentrated in the luxury segment. Buyers are increasingly interested in unique properties, often with irreplicable features, an area in which the available supply remains very limited and partly consists of properties with an inconsistent quality/price ratio.

In the mid-range segment—for Italian buyers—caution is still the prevailing sentiment, for three main reasons: i) the difficulty of finding properties that represent a real improvement in quality; ii) the wide variability in asking prices, which creates uncertainty, slows down decision-making, and fuels a cautious attitude; iii) a completely new geopolitical climate that is a source of apprehension and further caution. However, given that the trend of structural supply shortages has now lasted for at least five years, if the market were to see the introduction of truly high-quality residences, local demand would be ready to respond quickly and decisively.

The report indicates an improvementin the average absorption index —the percentage of properties sold compared to the total available—which reached 21.3%, marking an increase of 1.7 percentage points. Specific data for individual areas vary greatly, often due to the small size of the samples analyzed.

The picture was particularly positive in Quadrilatero, Centro Storico, and Venezia-Duse, while Brera and Magenta recorded lower performances, penalized by a less homogeneous stock offering and price expectations that were not always in line with the market, factors that made turnover more difficult.

In summary, quality is always the determining factor: high-end properties find buyers quickly, while less attractive ones remain unsold for longer: current demand in the Milan market is very selective and does not accept compromises.

The average time to sell has fallen slightly to 7 months. At the same time, the discount between the initial asking price and the final sale price has increased further, reaching 8.6% (an increase of 0.5% in the first half of the year and 1.4% year-on-year). This combination of factors is mainly due to owners being more willing to accept offers below the asking price, especially for properties that have been on the market for a long time or those with initial prices deemed unrealistic by buyers.

As a result, the average time unsold properties remain on the market has also decreased, falling below 26 months. Despite this reduction, this level remains very high, suggesting that owners need to make definitive decisions: either remove the property from the market or accept a significant price reduction.

The dynamics of asking prices confirm the trend consolidated since 2021, with fractional increases remaining around 1% per annum. The half-year under review shows differentiated growth: +0.85% for the average price, +0.64% for the average maximum, and +1% for the average minimum. Newly built or renovated properties recorded an appreciation of 0.9%; +0.75% for used properties in average condition or in need of renovation.

A significant factor concerns the gap between expectations and transactional reality: while asking prices rose by 1.5% on an annual basis, actual closing prices increased by a modest 0.1%, reflecting a 1.4% increase in discounts throughout 2025.

In the luxury segment (properties worth over €6 million), the maximum price per square meter for individual units shows different trends depending on the area: up in the historic center, Brera, Magenta, and other areas; down in Venezia-Duse; and just below parity in the Quadrilatero.

The average Top Price in the city (the maximum price requested in different areas of the city) continues to grow in 2025, albeit at a significantly slower pace than in previous years. The extraordinary upward trajectory that began in 2021—driven by a combination of international demand, for which these values represent a standard, and a speculative component on the part of sellers motivated exclusively by premium prices—has brought the city's maximum prices in line with those of competing metropolises.

The three most significant transactions during the period generated a total volume of over €23 million, with prices per square meter ranging from €18,000 to over €23,000.

The reasons for purchasing essentially confirm the distribution of the previous half-year: 57% of buyers are motivated by the need for a primary residence, 35% by replacement, while the investment component stands at 8%, penalized by the higher returns offered by alternative and more liquid assets such as equities and gold.

"Milan continues to exert a strong attraction on foreign investors," continues Marco E. Tirelli , "even though the peak in inflows was concentrated in the previous two half-years, in the wake of the abolition of the British 'Res non dom' regime. The increase in the flat tax, initially to €200,000 and then to €300,000 from January 2026, although a modest adjustment in relation to the assets of applicants, is likely to have a dampening effect on the number of applications from now on, simply because other countries have become more attractive than Italy. However, to offset this effect, we must consider the impact on the visibility of Italy and the city of Milan in particular resulting from the Winter Olympic Games.

The leases

After years of almost uninterrupted growth, demand in the first half of the year began to normalize across all segments: Mid-range (€40-90k per year excluding expenses), Top (€90-170k per annum excluding expenses), and Luxury (over €170k per annum excluding expenses). Demand for rental residences in the first half of the year was lower than in the two-year period 2023-2024.

This is a physiological readjustment after an expansionary phase that lasted at least five years and which, for the Top and Luxury segments, was mainly fueled by the attractiveness of the so-called "flat tax" regime. In these segments, demand comes mainly from two sources: on the one hand, the direct component—mainly foreigners, corporate expats, and international professionals looking for high-end solutions; on the other hand, the so-called "bridge demand," consisting of families who, unable to become buyers in a market with chronically insufficient supply, choose renting as a temporary solution while continuing their main search.

"In all segments, but particularly in the two upper segments," adds Torchiani, " the real critical issue in the sector remains on the supply side, such that demand, although less exuberant than in the past, continues to exceed availability. Truly exclusive residences, with strong visual impact and luxury amenities, are extremely rare on the market: the best solutions have already been absorbed by the wave of new residents who arrived in 2023 and 2024."

The combined effect of this is a market characterized by structural rigidity that keeps rents under upward pressure. In other words: fewer properties are being rented, but they are being rented at higher prices—a dynamic typical of markets characterized by the prevalence of scarcity value.

The semester closes with a seemingly counterintuitive figure:the lease absorption index rose to 35.6%, recording an increase of 0.8% compared to the previous period.

At first glance, this might seem like a sign of market vitality. In reality, this percentage improvement hides a double contraction: on the one hand, the number of contracts actually concluded has decreased; on the other, the supply itself has fallen even more sharply. The result is a "statistical optical effect" whereby two negative signs create a positive one.

The rental market is developing an increasingly polarized temporal geography, where the quality of the property determines radically different outcomes. Properties of real value are snapped up quickly, often in a matter of days or weeks, allowing owners to maintain their asking rents. The average time needed to conclude a lease has fallen slightly to 3.8 months. Not surprisingly, the average discount has fallen to 5.2% (-0.6% in the first half of the year).

In the mid-range segment, however, there is a clear distinction: if the contract is not closed within 3-4 months, it means that the property has weaknesses that are not attractive to the market (e.g., suboptimal location, poor maintenance, impractical layout).In these cases, the initial failure is often followed by a reduction in the asking price (around 15%), which only in a minority of cases makes the house more attractive. This is confirmed by the fact that the average time that empty apartments remain vacant is increasing to over 10 months. This accumulation reflects an inadequate supply that remains on the margins of the market, unable to attract tenants even in the face of progressively more favorable economic conditions.

Rental values continue on a controlled growth trajectory, with an average increase of 0.64%. However, it is at the top of the pyramid that the market is performing exceptionally well. Top rents —the maximum rent for a single residential unit—have exceeded the threshold of €750 per square meter per year throughout the city, with exceptional peaks of up to approximately €1,100 in the Quadrilatero district.

Three factors converge in sustaining these levels: the chronic shortage of premium supply, already analyzed above; the presence of international tenants for whom these amounts represent an established standard in their home markets; and, of course, the purchase prices of high-end residences—properties that combine iconic locations, high-end finishes, and exclusive services. Higher purchase prices result in higher rents.

It should be noted that this survey excludes short- and mid-term leases, which are managed by specialized operators with different pricing models. The fees for these formulas—which include ancillary services and integrated management—are not directly comparable with traditional 4+4 residential contracts and represent, in fact, a parallel market with its own dynamics.

Milan has consolidated its position as a global city, and data on the composition of rental demand confirms this: international tenants now account for around one-third of the total, a percentage that has been growing steadily in recent years.

However, segmentation by surface area reveals an even more marked geography: for residences of 300+ square meters, the presence of foreigners and Italian expats returning home has become almost exclusive. This segment now has codes and dynamics that are completely unrelated to the domestic market, operating according to the logic and benchmarks typical of major international capitals.

Forecasts for the first half of 2026

SALES: In the mid-range segment (1-3 million), the outlook for the coming months appears stable, although the turbulence in the global geopolitical and economic landscape could lead to further caution. Much in this segment will depend on the quality of the offering.

The top bracket (3-6 million) is where the coexistence of Italian and foreign buyers is most significant in numerical terms, and as mentioned, the two groups behave differently. While domestic buyers may slow down their purchasing decisions under the weight of the same macroeconomic uncertainties mentioned above, the international component—motivated mainly by tax advantages and stimulated by them to accelerate their purchasing decisions—is much less sensitive to these dynamics.

"The luxury segment (6+ million) continues to be a market unto itself," comments Tirelli, " fueled by international demand. In terms of number of transactions, this segment is insignificant compared to the overall market. Each transaction is (almost) unique and therefore linked much more to personal choices than to market dynamics. In general, further significant increases in asking prices do not seem likely, but we cannot rule out the possibility that the appearance of some exceptional homes on the market could generate front-page transactions."

Beyond the specific characteristics of each segment, however, a common thread emerges: market developments in the coming months will depend largely on the ability of suppliers to meet the quality standards demanded by an increasingly discerning and selective clientele.

LEASES: The picture that emerges is that of a mature rental market, which is transitioning from a phase of demand-driven expansion to a phase of consolidation conditioned by supply constraints. The stability of rents, in a context of reduced transaction volumes, suggests that Milan has reached a new plateau of values, supported more by limited supply than by intense demand.

"It is reasonable to expect this balance to stabilize," concludes Torchiani , "with some dynamics that deserve attention. In the Top and Luxury segments, international demand should continue to support rents at current levels, provided that new quality properties emerge. In the mid-range segment, pressure on rents could ease if, and only if, the supply of quality residences increases. Otherwise, the bottleneck on the supply side will continue to act as a protective floor for values, preventing sharp corrections even in less favorable scenarios."